Lessons from Alternative Accountancy: don’t sacrifice security in the rush to AI adoption

LIMA recently attended the Alternative Accountancy Technology Summit, where IT leaders from accountancy and audit firms got together to discuss the latest tech developments impacting the sector.

The trending topic at the event was – you guessed it – AI!

Speakers highlighted how adoption of AI in accountancy is already helping forward-thinking firms accelerate their operations and reduce internal costs. Which in turn reduces prices and increases demand for services.

Sprawling applications

Meanwhile, IT teams at many of the accountancy firms we spoke to at the event are battling with a huge number of applications for myriad different workflows and tasks. From onboarding clients, to running compliance checks to managing payroll – a typical practice uses 60 or 70 different apps within its day-to-day operations.

This app sprawl commonly includes SaaS, legacy and on-premise services. It throws up issues for IT teams around data duplication, security, credentials, permissions, training, technical complexity and cost.

Against the backdrop of this application sprawl, containing and controlling data becomes a greater challenge. With the introduction of AI tools to the mix, there is a risk that data could potentially be mishandled or inadvertently misused within AI systems, exposing your organisation to data leaks.

AI adoption

We’re not here to be the party poopers. AI is here and it’s having a massive impact in every sector. Those that refuse to adapt will be left behind. But there are ways to manage and control the use of AI in your organisation that doesn’t leave you exposed to major risk.

Here are just a few examples of how accountancy firms are adopting AI.

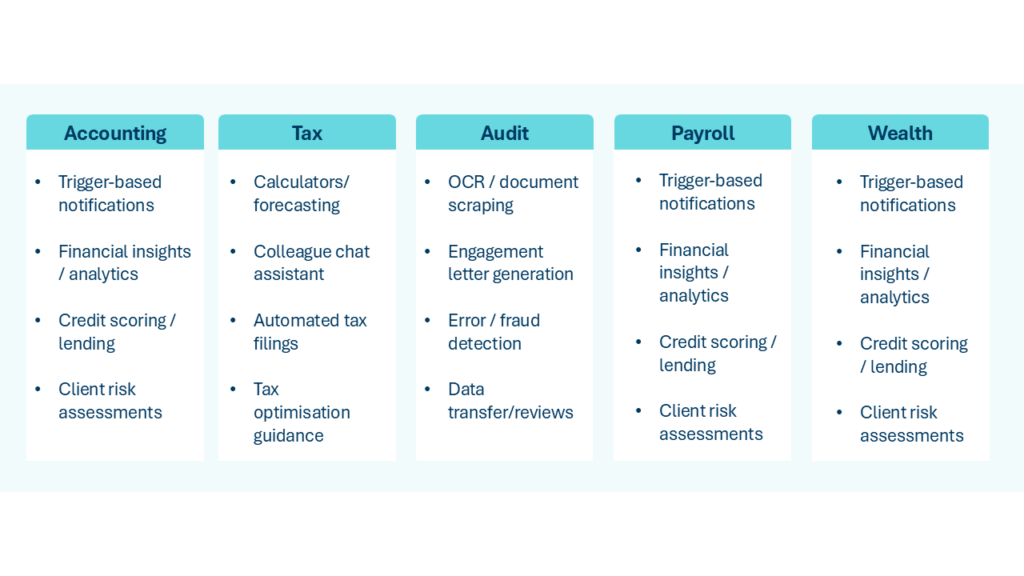

AI use cases in accountancy

Five ways to remain secure while adopting AI

1. Encrypt your data

Your systems process sensitive financial data. So it’s important that data is encrypted both at rest and in transit. This adds an extra layer of protection, preventing unauthorised access even if data is compromised. Using strong encryption protocols helps safeguard client information, especially in accounting.

2. Conduct regular system audits and risk assessments

AI systems should be continuously monitored to detect any potential vulnerabilities or breaches. Regular security audits and risk assessments can help identify and address weaknesses in security access, AI algorithms or integrations with other systems. By proactively assessing the risks, accountancy firms can mitigate the chances of data leaks or unauthorised access.

3. Adopt role-based access control (RBAC)

With AI systems processing vast amounts of sensitive data across multiple applications, it’s important to restrict access based on roles. Role-based access control ensures that only authorised employees can access or modify specific information. This helps prevent unauthorised viewing or manipulation of client data and ensures a clear trail of who accessed what data and when.

4. Prioritise compliance with data protection frameworks

Accountancy firms must comply with data protection regulations, and many choose to comply with frameworks like Cyber Essentials Plus to support their security and governance posture. When implementing AI, ensure the technology supports your compliance needs with these regulations, particularly in how personal and financial data is collected, stored and processed. There is great advice available from both the ICAEW and ACCA on this subject.

5. Train employees on data security best practices

Human error is often a leading cause of data breaches. It’s essential to train your staff on the importance of data security, particularly when using AI tools. Ensure they understand best practices, such as using strong passwords, recognising phishing attempts and understanding the risks and limitations of AI. Regular training can help employees be vigilant about security and reduce the risk of accidental data exposure.

Join our upcoming webinar, examining how IT teams in accountancy practices can revolutionise end user experience, strengthen security posture and help their organisations drive greater productivity and profitability.

Sign up here: WEBINAR: How are IT services driving better business outcomes for accountancy practices – LIMA – Insight-led IT services

LIMA offers a range of free assessments, including cyber resilience assessments and AI readiness assessments. We can help you on your journey to successful AI adoption.

With over 27 years’ experience supporting organisations with design and delivery of IT strategy, could LIMA be your perfect partner?

Contact the team at 0345 345 1110 or enquiries@lima.co.uk.